.jpg)

A capital hungry business will slowly break your heart.

Investing success comes down to just a few major things. Understanding the ongoing capital needs of an investment is at the top of that list.

Assets that require little to zero ongoing maintenance capital is the dream, but we’re not always so lucky.

There is bad CapEx and good CapEx:

- Bad CapEx = money spent fixing basic but essential parts of a business that frequently break.

- Good CapEx = capital projects that lead to increased profits at high returns on invested capital.

Real Estate CapEx

Investing in real estate helped crystallize this concept for me.

Because real estate capital improvements are pretty simple. Productive cap-ex adds profits (good) and maintenance CapEx makes you cry (bad).

Good CapEx for an apartment might be adding a clubhouse / fitness center that enables you to charge everyone higher rent.

Bad CapEx is a major plumbing leak that leads to a re-pipe of the entire property.

Because Susie in 3C is not going to pay more rent for new pipes, even if they’re gold plated. And considering where copper prices are today, those pipes might as well be gold.

A functioning plumbing system is a basic part of the core real estate “product”. Every tenant expects the plumbing to work flawlessly at all times.

And, they tend to freak out when such systems stop working. Don’t ask me how I know this.

Company CapEx

Chipotle adding a new store is an example of GREAT CapEx. The payback on a new store is around 2-3 years, which enables the firm to earn a remarkable ~35% on their invested capital. Someday they will saturate demand, but for now each new store prints cash.

Side note - When I was 26 and living on a balanced diet of 5 burritos a week, I wrote Chipotle corporate a mildly humorous letter begging them to let me franchisee some stores. They rebuffed my request. As a consolation, I got to keep the extra pounds from my extensive “due diligence”.

A well-executed vertical acquisition is also an example of good CapEx.

Bad CapEx is when a car company has a major recall. This erodes already thin profits. Every time I get a recall notice for some random non-essential part - aka the car sun Visor recall - I say a prayer for car company shareholders.

Great businesses use capital to fuel growth, while most burn capital to tread water.

The Perfect Business

If we accept this premise, then what is the perfect business model?

It’s a royalty business with built in pricing power.

This business requires nothing from you and yet the money keeps showing up in your mailbox in increasing amounts. This goes on for a unreasonable amount of time.

The Worst Business

The opposite of this is a giant manufacturing plant that:

- is filled with expensive and fragile equipment

- produces a commodity product in a highly competitive market at the thinnest of margins

- requires constant investments in R&D to improve the product just to maintain market share

- is also subject to extreme regulatory oversight

These type of companies are toxic investments that fool countless investors. Why?

Because they’re often important businesses with brand names that don’t look horrible (or expensive) on paper. They earn accounting profits but no actual cash because they are constantly pouring capital back into plant & equipment just to keep the lights on.

They frequently sucker value investors who think they’re getting a deal but are just subsiding management’s lavish compensation plans.

The real estate version of this is the 1970’s office or apartment building whose infrastructure is failing.

It’s not that you can’t make money from these type of investments, but you better make it quick.

Sooner or later the deferred maintenance has to be addressed. But in a hyper competitive market, buyers often have to overlook that CapEx to win the deal (then hope the systems don’t fail before they can exit).

Net Operating Income = EBITDA = Wishful Thinking

The worst companies and properties have something in common.

The profit & loss statement or net operating income look fine, but the cash flow statement is a dumpster fire.

How do companies and properties that burn cash survive?

- They capitalize EVERYTHING. Any minor repair becomes a cap-ex item and gets pulled OFF the income statement and thrown on the balance sheet. CLUE: balance sheet assets keep ballooning while cash keeps plummeting.

- The income statement “profits” allows them to consistently issue new shares (equity) and dilute existing shareholders.

- They sell to a greater fool on a multiple of EBITDA or Net Operating Income, dismissing all cap-ex as “one-time” non-recurring expenses (ex: WeWork’s “community-adjusted EBITDA”)

Plenty of firms get away with #1.

If a company capitalizes every light bulb replacement, that doesn’t necessarily make them Enron. The executive team is probably incentivized to play these games - stock option grants are often tied to profit margins or EBITDA growth. Frowned upon, but if the underlying business is great the investors will still do well.

#2 is far more concerning in my opinion - absent of major earnings per share growth or M&A deals, constant new share issuance is death by 1000 cuts. This is especially true when the stock is trading at a low historic multiple.

When that’s the case management should buyback their stock. If instead they choose to fire sell their equity (by issuing more shares), that’s a pretty clear sign they have a hidden cash flow problem.

In other words, management doesn’t have a choice.

I’ll add more on the share issuance / dilution topic in later post.

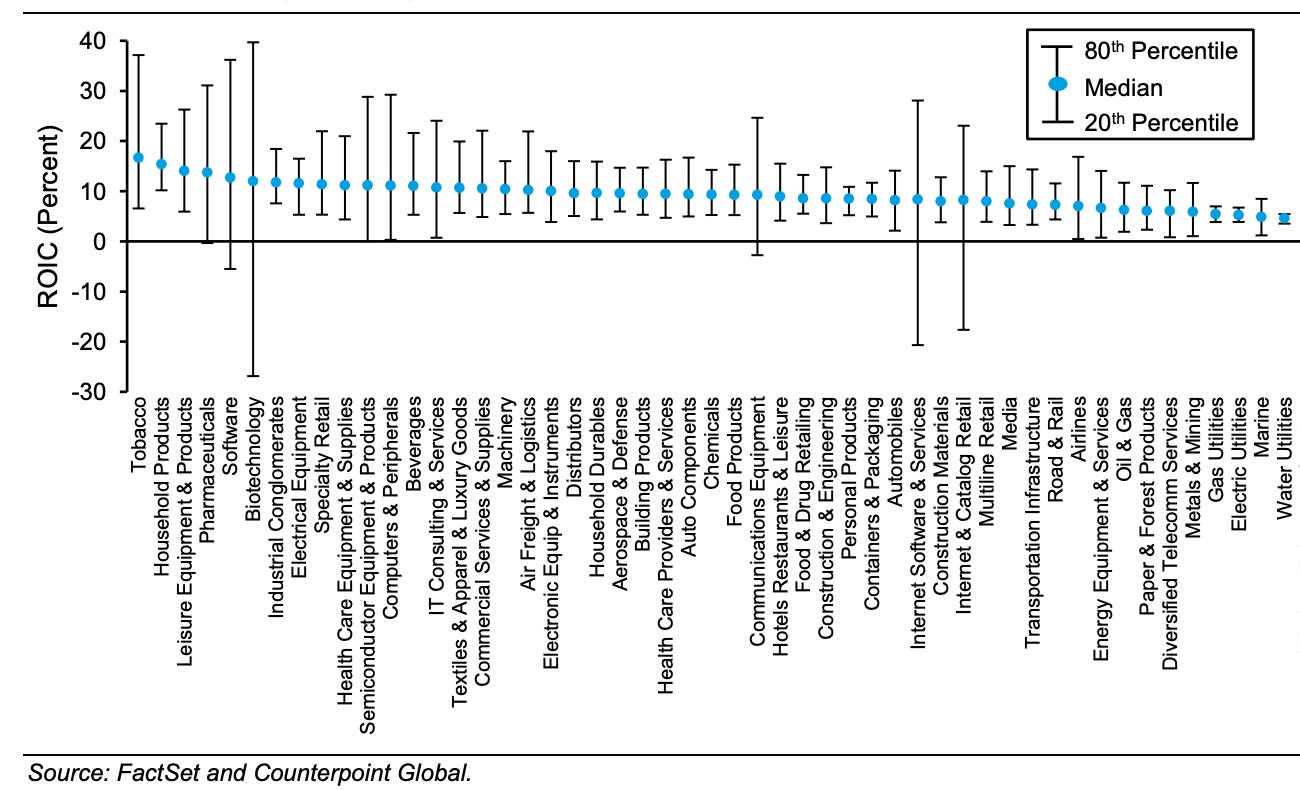

Low Maintenance CapEx = Higher ROIC

To hammer home this point, below are returns on invested capital (ROIC) by industry over the past 30 years. As you can see, industries on the left are heavy on intangible assets that don’t require much ongoing capital maintenance expenses.

Whereas, asset heavy industries on the far right such as utilities require constant upkeep and huge surprise capital maintenance outlays (often after a lawsuit).

This is why utility stocks high dividend payments are often fool’s gold.

ROICs by Industry for the Russell 3000, 1990-2021

Bottom Line

We care deeply about CapEx because we focus on long-term investing.

Over the short-term investors can get lucky and avoid capital problems. If you time the market right you can buy old and/or cheap assets with giant deferred maintenance, lipstick the pig and sell in couple years.

But if you want to own something for a LONG time, capital allocation is going to be responsible for a huge percentage of your returns.

You want that cash flow spent on growth not maintenance.